VAT on property transactions in the UK can be complicated, with different rules depending on the type of property, how it is used, and the nature of the transaction. Some property transactions are exempt from VAT, some are outside the scope of VAT, while others can be charged at 0%, 5%, or 20%.

Understanding the correct VAT treatment is extremely important to avoid unexpected tax bills, penalties, or cash flow issues with HMRC.

VAT on Residential Property

Sale of Residential Property

In most cases, the sale of residential property is exempt from VAT. This means no VAT is added to the selling price, and the buyer does not pay VAT on the purchase.

Residential Rent and Leases

Residential rents are generally exempt from VAT. Landlords normally do not charge VAT on rental income received from tenants.

However, if additional services are supplied separately, such as cleaning, maintenance, or concierge services, VAT may apply to those services.

New Build Homes

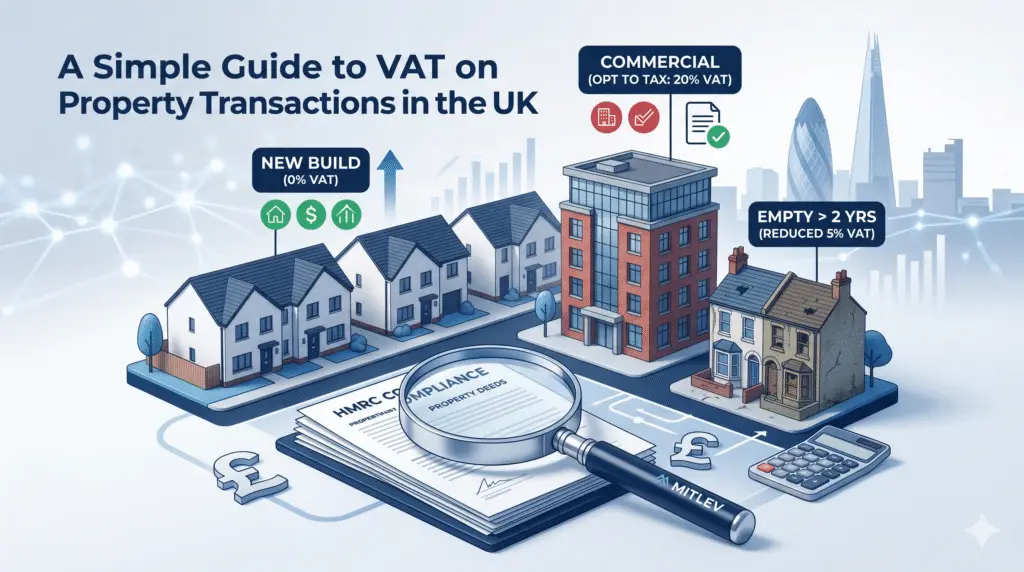

The first sale of a newly built qualifying home is usually zero rated for VAT purposes. This means the developer charges VAT at 0%.

Although no VAT is charged to the buyer, the developer can still recover VAT incurred on construction costs, which can create significant savings.

Construction and Renovation Costs

Building a new qualifying residential property is generally zero rated.

Most repairs and renovations to existing homes are standard rated at 20%. However, a reduced VAT rate of 5% may apply in certain situations, including:

- Converting a commercial property into residential dwellings

- Splitting one property into multiple flats

- Converting multiple flats into one home

- Renovating a property that has been empty for at least two years

These reliefs can create substantial VAT savings if structured correctly.

VAT Refunds for Self Builders

Individuals building their own home may be able to reclaim VAT on qualifying building materials through the DIY Housebuilders’ Scheme.

This is generally available to private individuals rather than VAT registered businesses.

At MITLEV Accountants, we regularly help property developers, landlords, and self builders understand which VAT reliefs are available and how to maximise VAT recovery while staying compliant with HMRC rules.

Holiday Lets and Serviced Accommodation

Holiday lets and serviced accommodation are usually treated differently from standard residential rentals.

Income from short term accommodation is generally subject to VAT at 20% if the activity amounts to a business and the VAT registration threshold has been exceeded.

This area often causes confusion, especially where Airbnb properties or mixed personal and business use are involved.

VAT on Commercial Property

Sale of Commercial Property

The sale of new commercial property is often subject to VAT at 20%.

Older commercial properties are normally exempt unless the owner has chosen to opt to tax the property.

Commercial Rent

Commercial rents are usually exempt from VAT by default.

However, landlords can choose to apply VAT by making an Option to Tax with HMRC.

Option to Tax

An Option to Tax allows the property owner to charge VAT on rent or sale proceeds. In return, the owner can usually recover VAT on related costs such as:

- Repairs

- Refurbishment costs

- Professional fees

- Purchase costs

This can be highly beneficial for commercial property investors and developers.

Once made, the option generally remains in place for 20 years, so professional advice is strongly recommended before making the decision.

The option to tax normally does not apply to residential parts of mixed use properties.

At MITLEV Accountants, we advise clients on whether an Option to Tax is beneficial, assist with HMRC notifications, and help avoid costly VAT mistakes during property purchases and sales.

Transfer of a Going Concern (TOGC)

In some cases, the sale of a tenanted commercial property may qualify as a Transfer of a Going Concern.

If the conditions are met, the transaction can fall outside the scope of VAT entirely.

This can produce major cash flow advantages for buyers because VAT does not need to be paid upfront on the purchase price.

Strict conditions apply, including VAT registration requirements and, in some cases, an Option to Tax being in place.

SDLT and VAT

Where VAT is charged on a property purchase, Stamp Duty Land Tax is usually calculated on the VAT inclusive amount.

This means VAT can significantly increase the overall SDLT bill.

Understanding the VAT position before completion is therefore essential.

Partial Exemption and Property Businesses

Property VAT can become more complicated when a business has a mix of VATable and non VATable income.

This is known as partial exemption.

A common example is a landlord who:

- Charges VAT on a commercial property

- Does not charge VAT on residential rental income

Because the business has both types of income, it usually cannot reclaim all of the VAT on its costs.

Taxable Income

Taxable income is income where VAT is charged. This includes income charged at:

- 20% VAT

- 5% VAT

- 0% VAT

Even if VAT is charged at 0%, it is still treated as taxable income for VAT purposes.

If costs relate directly to taxable income, the VAT on those costs can usually be reclaimed in full.

Exempt Income

Exempt income is income where no VAT is charged.

Residential rental income is one of the most common examples.

If costs relate directly to exempt income, the VAT on those costs usually cannot be reclaimed.

Shared Costs

Some business costs relate to both taxable and exempt activities. For example:

- Accountancy fees

- Utilities

- General repairs

- Office costs

In these situations, only part of the VAT may be reclaimable. The business normally needs to work out a fair percentage split as per HMRC guidelines.

Small Amounts of Exempt VAT

HMRC allows businesses to reclaim exempt related VAT if the amount is very small.

This is called the de minimis rule.

Broadly, the exempt related VAT usually needs to be:

- Less than £625 per month on average

- Less than half of the total VAT incurred

If both conditions are met, the business may still be able to reclaim all of its VAT.

Partial exemption calculations can quickly become complex, especially for landlords, developers, and mixed use property businesses.

At MITLEV Accountants, we help property businesses work out how much VAT can be reclaimed, prepare partial exemption calculations, and ensure the correct VAT treatment is applied to avoid HMRC issues later on.

Why Professional VAT Advice Matters

The VAT treatment of property transactions should always be reviewed before contracts are exchanged or work begins.

Getting advice early can help:

- Avoid costly HMRC errors and penalties

- Improve cash flow

- Maximise VAT recovery

- Ensure the correct VAT treatment is applied from the outset

Property VAT is one of the more technical areas of UK taxation, and even small mistakes can become expensive. Proper planning can make a significant financial difference for landlords, investors, developers, and property businesses.